Digital payment systems remained the main drivers of financial inclusion in the emerging economies, transforming individuals’ access to small and large financial services. Via mobile phone-based technology, electronic wallets, and blockchain-type systems, the payment systems introduced tens of millions of people into formal financial conduct, fueling economic empowerment and poverty reduction in 2025.

Why Financial Inclusion Matters

Financial inclusion—the presence of and access to the right financial services at low cost and in a timely fashion—is the gateway to sustainable economic development and income convergence. The majority of people in developing nations are excluded from the formal financial system based on geographical, economic, and social barriers.

Electronic payment systems address all these problems by developing low-cost, scalable payment infrastructure for insurance, credit, and savings products for micro-enterprises, rural villages, and inaccessible women to access mainstream banks.

Drivers of Digital Financial Inclusion

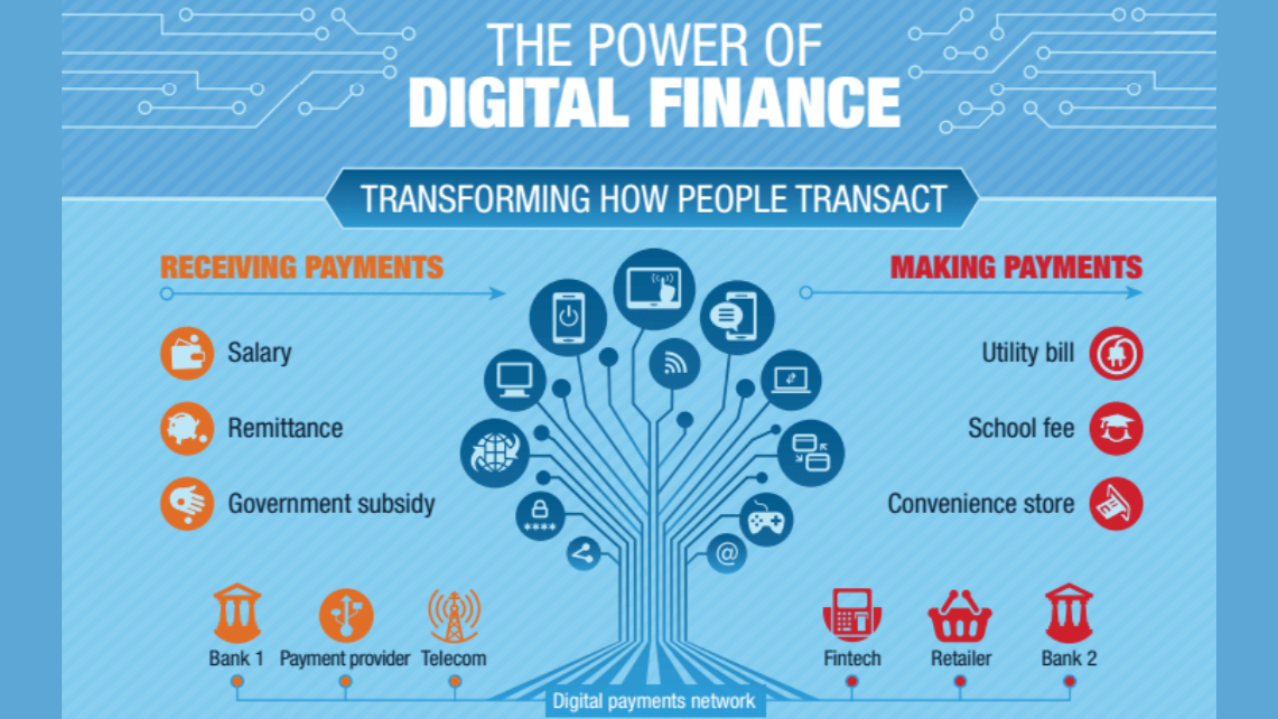

- Mobile and Internet Infrastructure: Its expansion of mobile networks, even into rural areas, has played a key role. Feature phones constructed using USSD codes made it possible, with smartphone capabilities offering more. The M-Pesa example in Kenya illustrates the capability of mobile technology in pushing financial services to the mass market.

- Digital Identity Systems: Secure digital identity systems like India’s Aadhaar biometric identification enable it to be secure and effective to open accounts and obtain financial services through user authentication.

- Regulatory Frameworks and Public Policy: Governments coming in with regulatory sandboxes, consumer protection, and pro-fintech public policy assurances of availability of innovation and trust settings.

- Social Inclusion and Gender Programs: Financially inclusive products and customized financial education bridge the gender and social exclusion gap.

- Energy System and Data Security: Reliable electricity supply and internet with appropriate data security and cybersecurity are essential.

Economic and Social Impacts

There is proof to provide that electronic payment systems nudge saving rates higher, extend availability of credit, facilitate remittance and allow for cash transfer, which is also the strand of economic resilience. Financially included consumers also spend more money on business classes, education, and health, generating positive feedback loops for societies.

Secondly, e-finance is a development enabler that fosters micro, small, and medium-size enterprises, which form the backbone of most developing countries’ economies.

Challenges and Opportunities

Despite upgrading, digital illiteracy limitations, infrastructural inadequacies, cybercrime, and very deep-seated poverty bring extension to a standstill on a large scale. Direct intervention by government, private sector, and development partners is needed to fill gaps.

Encouraging low-cost phone usage, people’s own-initiative digital literacy, and more effective data protection legislation are also at the top.

Conclusion

The electronic payment system has the top priority for funding more financial services and inclusiveness of growth in the new economy. Electronic payment systems create new economic chances for the poor to break through current obstacles, and accelerate poverty reduction and socio-economic progress.

Until 2025, sustained commitments toward digital infrastructure, enablement policies, and overall strategy will be required in order to unlock the power of digital payments financial inclusion and more resilient and more inclusive economies for all.