For years, if you needed a loan, you went to the bank. Simple, regulated, sometimes mind-numbingly slow. But today, thanks to the internet, millions are bypassing the middleman entirely, opting instead Peer-to-Peer (P2P) Lending.

P2P lending sites, like LendingClub or Zopa, are essentially places where they put borrowers or business entities seeking funds in front of lenders who possess the funds to lend. Such simple innovation is not only a fantastic new way of borrowing; it’s a disruptive force redesigning the credit market old-fashioned and carving itself out of the banks’ own lending business.

The P2P Promise: Efficiency and Access

The inherent appeal of P2P websites is the promise of increased efficiency and transparency.

For the Borrower: Faster and Better Rates

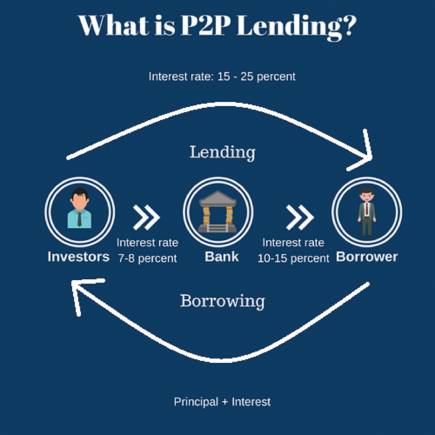

By cutting out the expensive overhead of bank branches, tellers, and legalistic regulatory red tape, P2P sites are able to offer borrowers lower interest rates than comparably priced personal loans or credit cards. Application time is also typically faster, relying substantially on computer programs for assessing risk. Competitiveness and speed have made the P2P sites consumers’ sweetheart source of funds for individuals needing debt consolidation or small businesses needing immediate capital to fund growth.

For the Investor: Greater Returns

On the other hand, P2P lending enables investors (or “lenders”) to earn greater returns than a low-interest savings account or bond. Investors may divide their risk and diversify by putting small amounts of money into dozens or hundreds of individual loans. They act as a mini-bank.

Risk-Return Profile

Even though returns are lucrative, P2P websites expose an investor to a special type of risk other than bank accounts:

1. The Risk of Default

The biggest risk to investors is default. P2P investments are not insured by government agencies (e.g., the FDIC in the US) like deposits in banks. When there is default by the borrower, the risk is borne by the investor. Platforms balance this risk by charging variable interest rates based on the credit rating of the borrower—low credit rating pays a premium rate that compensates the investor with higher returns for the greater risk (risk-return trade-off).

2. Uncertainty of Algorithms

P2P lending relies on internal models and algorithms of risk. Although the algorithms can process large data sets well fast, the models could never have been tested during record economic downturns. Default rates within the portfolio are going to rise at a rapid rate if a risk model of a platform is faulty or a platform underestimated a systemic economic event.

3. Liquidity Risk

P2P investments are not as liquid as bank deposits. If an investor needs to access his money in a hurry, he cannot just withdraw it. He will have to wait till the loan matures or sell his portion in a secondary market, discount.

The Impact on Traditional Bank Lending

The rise of P2P lending has also had a practical effect on the functions of the incumbent banks, mainly in making them more competitive and efficient and innovative.

- Softer Lending Standards (The Good Pressure): P2P websites are best positioned to lend to those consumers who might just miss the strict standards of the big banks (e.g., those with poor credit or non-traditional incomes). In order to avoid loss, banks usually have to ease and look slightly at their own stringent lending standards, particularly on consumer credit and small business loans. It is consumer-friendly because it makes credit more accessible.

- Going Digital: Banks have been forced to computerize their own loan origination processes. Banks have adopted such as algorithmic risk assessment and automated underwriting technology developed by P2P companies in an attempt to be able to accelerate application processing timelines as well as reduce their operating costs.

- A Differentiation Catalyst: With P2P existing, banks are forced to focus on those domains where they continue to have a winning position, i.e., providing cutting-edge products, wealth management, or FDIC-insured deposits, thereby shifting the competitive landscape.

Short of that, P2P lending has introduced much-needed efficiency and competition to the credit market. Even while bearing more default and liquidity risk, overall effect has been to expand access to credit and induce traditional finance institutions to innovate more, driving the system along faster and internationally.